What is an Electronic Contract? Definition, Types, and How Businesses Manage Them at Scale

Last updated: July 9, 2026

Most organizations have already solved the signing problem. The problem is everything before and after the signature.

Contracts get stuck in approval loops for weeks. Legal teams cannot tell which version is current. Procurement misses auto-renewal windows. Sales deals stall because an agreement is sitting in a legal queue with no visibility into its status. Electronic contracts alone do not fix these problems.

An electronic contract, or e-contract, is a legally binding agreement created, negotiated, and signed entirely in digital form. It carries the same legal weight as a handwritten paper contract under the ESIGN Act in the USA, UETA across 49 states, and eIDAS across EU member states, provided it satisfies three core requirements: offer, acceptance, and consideration.

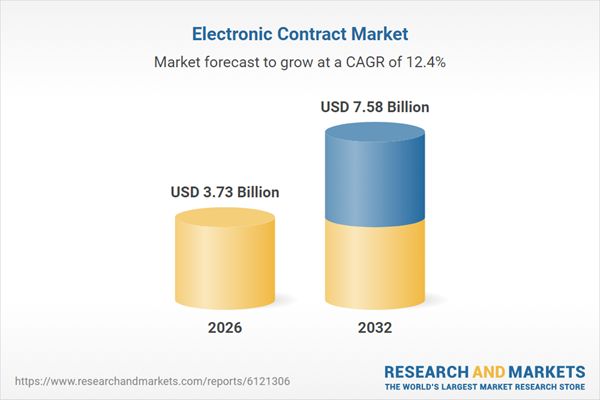

The Electronic Contract Market is on a strong growth trajectory, expanding from USD 3.35 billion in 2025 to USD 3.73 billion in 2026, and expected to rise at a CAGR of 12.37% to reach USD 7.58 billion by 2032. [Research and Markets]

This page covers what makes an e-contract legally enforceable, how they work in practice, the four main types, the real operational challenges at scale, and what a contract management system must do to solve them.

What is an electronic contract?

An electronic contract is a legally binding agreement where every stage, from drafting and negotiation to approval and signing, takes place digitally. It works identically to a paper contract under law.

For an e-contract to be enforceable, it must contain the same legal elements as any valid contract. Missing one makes the agreement challengeable in court.

1. Offer

One party proposes specific, definite terms and communicates them to the other party. A vague proposal does not constitute a valid offer. The terms must be clear enough for a court to determine what the parties agreed.

2. Acceptance

The other party agrees to the exact terms as stated. In an e-contract, acceptance is recorded through a digital signature, a “click to accept” action, or a typed name. A counter-proposal is a rejection of the original offer. The negotiation resets.

3. Consideration

Both parties exchange something of value: money, services, goods, or a binding promise to act. Consideration is what separates a contract from a non-binding agreement or a favour.

4. Mutual consent

Both parties understand the terms and agree to them of their own accord. Contracts signed under duress, misrepresentation, or fraud are void, regardless of the electronic signatures applied to them.

5. Legal capacity

The contract signatory must have the legal authority to bind the organisation. An authorized signatory is the person formally designated to execute agreements on behalf of a company. Contracts signed by someone without that authority are unenforceable against the organisation, regardless of their seniority.

6. Legal purpose

The agreement must comply with applicable law. A contract for an illegal activity is void regardless of how it is formed or what signatures it carries.

7. Electronic signature

The digital mechanism that authenticates each party’s identity and records their agreement. E-signatures range from a typed name to a cryptographic certificate issued by a trust authority. For the distinction between e-signatures and digital signatures, see digital signature vs electronic signature.

8. Audit trail

A timestamped, tamper-evident record of every action taken on the contract: who accessed it, when, from which IP address, and when each party completed their signature. Paper contracts cannot produce this level of verification. In disputes or regulatory audits, the audit trail is the primary evidence of what happened and when.

How electronic contracts work in modern businesses

In any organization managing contracts at scale, an e-contract moves through a defined workflow involving multiple teams, approval hierarchies, and compliance checkpoints before anyone signs.

A standard e-contract workflow covers six stages:

- Contract drafting: Legal teams use standardized templates and pre-approved clause libraries to create the initial document. Contract drafting tools reduce time on routine, low-risk agreements and let legal focus on complex negotiations.

- Redlining and negotiation: Both parties propose and accept changes in a tracked redlining environment. Contract negotiation software records every edit, so legal teams know which version is the latest approved draft. The system flags clause deviations from the standard template before the contract moves forward.

- Approval routing: The contract routes through a predefined approval hierarchy (legal, finance, leadership) based on contract type, value, and risk level. Contract approval workflows eliminate the manual email chains that stall deals for weeks.

- Execution: The final version is sent for electronic contract signing. Each signatory completes their action on the platform, which records the timestamp, IP address, and authentication method used. The platform locks the signed document and its full audit trail.

- Obligation tracking: After execution, AI contract review tools extract key metadata (payment terms, SLAs, termination clauses, liability caps, renewal dates) so commitments do not get buried inside a signed PDF.

- Repository and search: Executed contracts go into a centralized contract repository. Legal ops and procurement teams search by party name, clause type, value, or expiry date in seconds rather than searching through email folders and shared drives.

This end-to-end workflow separates organizations using CLM from those that digitized only the signature step.

See how HyperStart manages e-contracts end to end

HyperStart CLM covers the full electronic contract lifecycle: drafting with pre-approved clause libraries, automated approval routing, AI-powered contract review, and post-signature obligation tracking. Legal, procurement, and finance teams deploy it in four weeks.

Book a DemoHow do electronic contracts differ from traditional paper contracts?

The gap between the two is not the signature method. It is everything that controls a contract before and after signing: approval cycles, version tracking, obligation management, and audit readiness.

A manufacturing enterprise managing 2,000 supplier contracts across procurement, logistics, and production cannot track versions, renewal dates, or compliance obligations on paper. Legal cannot confirm which version of a vendor agreement is current. Procurement cannot tell which contracts are approaching auto-renewal. Operations cannot verify that supplier SLAs are being met against the signed terms. Electronic contracts solve the signing problem. CLM software solves everything after it.

1. Execution time is the most visible difference. A standard vendor agreement averages 22 days to close on paper — print queues, courier delays, wet-ink chasing, and re-scan cycles eat that time (WorldCC, 2023). The same agreement closes in under 24 hours with automated routing and electronic contract signing.

2. Version control is where paper contracts create the most hidden risk. When redlines travel through email, teams lose track of which version is current. A supplier and a buyer often end up working from different drafts without realising it. Electronic contracts timestamp every edit and attribute every change to a specific party. There is always one authoritative version.

3. Approval workflow determines how fast deals close. Paper contracts move through legal, finance, and leadership by email. Each handoff introduces delay and zero visibility for the team waiting. Contract approval workflows route documents based on type, value, and risk, with a live status trail at every stage.

4. Audit trail is the difference that matters most in regulated industries. A paper contract cannot tell you who reviewed which clause, when they approved it, or from which location the signature was applied. An electronic contract records every action, timestamped, tamper-evident, and exportable on demand. In a compliance audit or supplier dispute, this record determines the outcome.

5. Obligation tracking is where contract value leaks without anyone noticing. A supplier agreement auto-renews at the original price because no one caught the 60-day renegotiation window. A maintenance contract expires unnoticed because it was filed and forgotten. Electronic contract management systems track every renewal date, SLA window, and payment milestone, and alert the right team before the deadline closes.

| Factor | Electronic contract | Traditional paper contract |

|---|---|---|

| Signing method | Digital signature, clickwrap, or typed name; each timestamped and attributed to the signing party with a verifiable record | Wet signature requiring physical presence or courier delivery; no verification record beyond the signed page |

| Execution time | Under 24 hours with automated approval routing and e-signature; no printing, scanning, or courier wait | 22-day average; print queues, courier delays, manual signature chasing, and re-scan cycles account for most of the time |

| Version control | Every redline tracked and attributed to a specific party; one authoritative version exists at all times and is accessible to all permitted parties | Multiple draft attachments circulating in email threads; no reliable record of which version is current or who last approved a specific change |

| Approval workflow | Routes automatically to legal, finance, and leadership based on contract type, value, and risk; each approver receives a notification and acts within the platform | Manual email forwarding with no status visibility; contracts sit in inboxes for days with no way to see who holds the document or where the delay is |

| Storage | Centralized, searchable repository with role-based access, full version history, and retention controls | Physical filing cabinets and unstructured shared drives; no consistent retrieval method, no access control, no version history |

| Audit trail | Timestamped record of every action: who accessed the contract, when, from which device, and when each party applied their signature | Manual logs or no record; no verifiable chain of custody showing who reviewed which clause, when they approved it, or from which location the signature was applied |

| Obligation tracking | Automated alerts before renewal dates, SLA windows, payment milestones, and termination deadlines; no manual calendar entry required | Manual calendar entries that are missed when staff change, workloads peak, or the person who created the reminder leaves the team |

| Cost per contract | Average saving of $20 per contract; eliminates printing, couriering, scanning, and physical storage overhead entirely | $20+ per contract in print, postage, scanning, and admin costs; at 1,000 contracts per year that is $20,000 in direct overhead before legal processing time |

| Legal validity | Valid under ESIGN Act (USA), UETA (49 US states), eIDAS (EU), and IT Act 2000 Section 10A (India) | Universally accepted across all jurisdictions; this is the narrowest operational gap between the two formats |

| Search and retrieval | Full-text search by clause text, party name, date range, or contract value; a specific commitment surfaces in seconds from any device | Manual search through filing cabinets or email threads; locating a specific clause or obligation in a filed contract takes hours and often fails |

Legal validity shows the narrowest gap. Both formats hold up in court for most contracts. Every other row is where paper contracts fail teams managing contracts at scale.

A wet-ink signature is still required for a narrow category of documents in some jurisdictions: wills, certain powers of attorney, and specific real estate deeds. For every other standard business contract, electronic contracts are legally accepted.

Types of electronic contracts

Not all e-contracts use the same acceptance mechanism. The legal strength of an electronic contract depends on which type applies and how clearly the offering party presented the terms before acceptance.

1. Clickwrap agreements

The user checks a box or clicks “I agree” to confirm acceptance. Courts consistently uphold clickwrap contracts because acceptance is affirmative, deliberate, and recorded at a specific timestamp. Clickwrap is the most legally defensible type for SaaS platforms, software subscriptions, and service agreements.

2. Browsewrap agreements

Terms are posted on a website, and using the site constitutes acceptance without any explicit confirmation. Courts have repeatedly struck down browsewrap agreements where users had no clear notice of the terms. Browsewrap carries significant enforceability risk for high-value or high-risk agreements and should not be relied on without legal review.

3. Scrollwrap agreements

The acceptance button activates only after the user scrolls through the full terms. Stronger than browsewrap because the platform confirms the user reached the end of the document. Weaker than clickwrap because it does not require a separate affirmative action beyond scrolling.

4. Sign-in wrap agreements

Acceptance is implied when a user creates an account, with terms referenced during signup. Enforceability depends on how clearly the platform displayed the terms during registration. Courts have rejected enforceability where users could complete registration without encountering the terms at all.

Are electronic contracts legally binding?

Yes. Electronic contracts are legally binding in most jurisdictions when they meet the same formation requirements as paper contracts. The legal framework varies by region:

- USA: The ESIGN Act (2000) gives e-contracts the same legal effect as paper at the federal level. UETA, adopted by 49 US states, provides parallel protection at the state level. Both laws require that parties consent to do business electronically.

- Europe: The eIDAS Regulation recognizes three tiers of electronic signatures across all EU member states: simple electronic signatures (SES), advanced electronic signatures (AES), and qualified electronic signatures (QES). Higher-risk contracts require higher-tier signatures to be enforceable.

- India: Section 10A of the IT Act 2000 states that contracts formed through electronic means are valid and enforceable, provided they satisfy standard contract formation requirements.

- United Kingdom: The Electronic Communications Act 2000, confirmed by the Law Commission’s 2019 guidance, validates electronic signatures for most standard business contracts.

Enforceability also depends on the contract type. A clickwrap agreement with a recorded digital signature and complete audit trail is the most defensible in court. A browsewrap agreement with no affirmative acceptance is the weakest and the most frequently challenged.

For a breakdown of signature types and their legal standing by jurisdiction, see digital signature vs electronic signature.

What are the benefits of electronic contracts?

Electronic contracts reduce contract cycle times by up to 80% and help organizations recover an average of 9% in annual revenue lost to poor contract management (WorldCC, 2023). The benefits compound across every team that touches a contract.

1. Faster contract cycle times

E-contracts reduce contract cycle time by up to 80% compared to paper-based processes (WorldCC, 2023).

A vendor agreement that takes 22 days on paper closes in under 24 hours with automated approval routing and electronic contract signing. In manufacturing, where procurement teams process hundreds of supplier purchase orders per quarter, that speed difference directly affects production timelines. A delayed supply agreement holds up the entire procurement cycle. Automated routing removes every manual handoff from the process.

2. Lower cost per contract

Organizations save an average of $20 per contract by eliminating printing, couriering, scanning, and physical storage costs.

At 500 contracts per year, that is $10,000 in direct overhead savings before factoring in legal and administrative time recovered. For manufacturing enterprises processing thousands of supplier and logistics agreements annually, the savings scale with contract volume. A company running 5,000 contracts per year saves $100,000 in direct costs alone, without counting the legal hours freed from manual processing.

3. Tamper-evident audit trail

Every e-contract maintains a timestamped record of every action: who accessed it, when, from which device, and when each party signed.

In disputes and regulatory audits, the audit trail is the primary evidence. Paper contracts cannot produce a chain of custody showing who reviewed which version and when. For regulated industries — healthcare, financial services, manufacturing — audit readiness is not optional. It determines whether a company can prove compliance during an inspection or respond to a supplier dispute without spending weeks reconstructing what was agreed and by whom.

4. Real-time visibility into every contract

Electronic contract management systems show exactly which contracts are in progress, where they are in the workflow, and which approvals are outstanding.

Leadership can measure cycle times and bottlenecks in real time. Contract intelligence replaces the manual process of emailing stakeholders for status updates. Operations and finance teams see upcoming commitments before they become obligations past due. For procurement leaders overseeing supplier networks, this visibility converts contract data from a static archive into an operational dashboard.

5. Remote signing across borders

Parties in different countries sign the same document at the same time.

Sales teams close deals without geography delaying the process. Procurement teams onboard international vendors without physical handoffs. In global manufacturing supply chains, where a single production line depends on suppliers across multiple continents, remote signing eliminates the courier delays that previously held agreements up for days. A component supplier in Vietnam and a procurement team in Germany sign the same agreement within the hour.

6. Automated renewal and obligation alerts

Teams eliminate missed renewals, a primary source of contract value leakage, with automated alerts that fire before renewal dates, payment milestones, and SLA windows.

WorldCC estimates that poor contract management costs organizations an average of 9% of annual revenue (WorldCC, 2022). A significant portion of that leakage comes from contracts that auto-renew at unfavourable terms because no one flagged the renewal window in time. Electronic contract management systems track every expiry date and alert the right team before the window closes — whether that is a software subscription, a supplier agreement, or a manufacturing maintenance contract covering critical equipment.

Challenges of managing electronic contracts at scale

Organizations that digitized signing but not the full contract lifecycle face the same operational problems as paper-based teams. Contract visibility, governance, and risk exposure remain unsolved.

1. Legal teams

- Contract versions scattered across email threads with no clear record of which is the latest approved draft.

- High volumes of low-risk, routine agreements consuming legal bandwidth that should go to complex negotiations.

- Clause deviations during redlining go undetected because teams track changes in document comments rather than a system that flags non-standard language.

- Legal teams cannot locate contracts during audits or disputes. Contract discoverability fails without a centralized repository.

- Post-signature obligations, liabilities, and commitments go untracked the moment a contract is signed and filed. Legal exposure accumulates without visibility.

- Regulatory changes require amendments across hundreds of agreements, with no way to identify which contracts are affected without reading every one.

2. Procurement teams

- Vendor onboarding stalls because supplier contracts sit in approval queues with no automated routing or visibility into who is holding them.

- Supplier contracts stored across email, shared drives, and procurement systems with no single source of truth.

- Missing auto-renewal dates lead to unwanted renewals or missed renegotiation windows, a direct form of contract value leakage.

- No centralized view of negotiated pricing, volume discounts, and service terms across active supplier agreements. Teams cannot compare terms or enforce commitments.

- Vendor compliance obligations (audit rights, data processing terms, insurance requirements) go untracked after contract execution.

3. Sales teams

- Deals stall because contracts spend weeks in legal review with no status visibility for the sales rep or the customer.

- Repeated redlining cycles delay revenue recognition and extend the quote-to-signature cycle beyond what the deal economics can support.

- Sales reps spend time searching for approved contract language, redlines, and fallback clauses instead of running the deal.

- Customers push back on terms during negotiation with no structured deal desk workflow to manage escalations or approve deviations.

4. Compliance and risk teams

- No reliable audit trail proving who approved what and when, which leaves teams exposed during regulatory audits and litigation.

- Inconsistent contract language across departments because teams use their own templates without a governed clause library.

- Contractual obligations buried inside signed PDFs remain untracked after execution, creating unmanaged liability.

- No systematic way to enforce contract governance or policy compliance across legal, procurement, and sales.

5. Operations and leadership

- No visibility into how many contracts are active, where they are stalled, or which commitments are approaching their renewal window.

- Contract cycle times, approval bottlenecks, and throughput cannot be measured without contract analytics.

- Revenue, vendor, and legal commitments are trapped in unstructured documents across multiple systems, making forecasting unreliable.

Stop managing contracts in email threads

HyperStart CLM centralizes drafting, negotiation, approval, signing, and obligation tracking in one platform. Legal, procurement, sales, and finance teams get full contract visibility, without email chains, missed renewals, or version confusion. Deploys in four weeks.

Book a DemoWhy businesses use CLM software to manage electronic contracts

Electronic contracts create operational value only when the full lifecycle is managed. Basic e-signing tools cover the signature step. Digital contract management software covers everything else:

- Centralized contract repository: One searchable system replaces email folders, shared drives, and filing cabinets. Every contract version, amendment, and related document lives in one place, accessible by role-based permission.

- Automated approval workflows: Contracts route to the right stakeholders based on type, value, and risk level. Approval hierarchy is enforced by the system, not by manual follow-up.

- AI contract review: AI-powered tools extract metadata, flag clause deviations from standard templates, and highlight contract risk before execution. Legal teams review high-risk exceptions; routine contracts process without manual intervention. See how AI-powered contract management works in practice.

- Obligation and renewal tracking: After execution, CLM software tracks every commitment (payment terms, SLAs, renewal windows, termination rights) and alerts the right team before a deadline passes.

- Contract analytics: Leadership gets real-time data on cycle times, bottleneck stages, contract volume by team, and renewal exposure. Contract intelligence replaces manual reporting.

- Compliance and audit readiness: Every action on every contract is recorded. During audits or disputes, legal teams produce a complete chain of custody in minutes.

Key features to look for in an electronic contract management system

Not every CLM platform covers the full contract lifecycle. Evaluating an electronic contract management system means checking whether it covers these capabilities:

- Clause library and template management: Pre-approved, standardized templates that reduce drafting time and limit clause deviations across the organisation.

- Redlining and version control: Every change tracked and attributed to a specific party. No ambiguity about which version is the latest or which redline was accepted.

- Automated approval routing: Rules-based routing by contract type, value, and risk level. No manual forwarding and no deals held up because someone forgot to pass the document on.

- Native e-signature or integration: Contract signing built into the platform or integrated with a verified e-signature provider, with a complete audit trail attached to every executed document.

- AI contract review and metadata extraction: Automated identification of key terms, obligations, missing clauses, and risk flags before execution.

- Full-text contract search: Search across all contracts by clause text, party name, date range, value, or custom metadata in a centralized repository.

- Obligation and renewal tracking: Automated alerts before renewal dates, payment milestones, SLA windows, and termination deadlines.

- Contract analytics and reporting: Dashboards showing cycle times, approval bottlenecks, contract volume by team, and upcoming expirations.

- Role-based access controls: Teams see and act on only the contracts relevant to their role. Sensitive terms are not visible across the entire organisation.

- System integrations: Connections to CRM, ERP, procurement, and HRIS platforms so contracts connect directly to the business data they govern.

Examples of electronic contracts

E-contracts appear across every business function and industry. Common examples include:

- SaaS terms of service: A user who clicks “I agree” during account signup forms a binding clickwrap contract with the software provider.

- Employment agreements: Offer letters, NDAs, and non-competes sent and signed via e-signature platforms before a candidate joins, with full audit trail documentation.

- Vendor and supplier contracts: Procurement agreements managed end to end, from initial negotiation and redlining to renewal alerts and obligation tracking.

- Real estate purchase agreements: Buyers and sellers sign purchase contracts electronically under state-level UETA provisions in the USA.

- B2B sales contracts: Master service agreements (MSAs), statements of work (SOWs), and order forms processed through CLM platforms connected to CRM systems.

- Financial agreements: Loan documentation, credit agreements, and banking contracts issued and signed electronically, cutting closing timelines from weeks to days.

- HR and contractor agreements: Employee onboarding documentation, independent contractor agreements, and consulting contracts managed at volume by HR teams.

Manage electronic contracts end to end with HyperStart

HyperStart is a contract lifecycle management platform built for legal, procurement, finance, and HR teams at mid-market and enterprise companies. It manages every stage of the e-contract lifecycle: drafting with pre-approved clause libraries, AI-powered contract review, automated approval routing, electronic contract signing, and post-signature obligation tracking.

Contracts are stored in a centralized, searchable repository with role-based access, renewal alerts, and a full audit trail on every document. Use contract signing software built for teams managing contracts at volume.

HyperStart deploys in four weeks.

Frequently asked questions

IN THE ARTICLE

Try first. Subscribe later.

Boost your legal ops efficiency by 80%.