Payment Agreement Template

Get a ready to use payment agreement template to clearly define payment schedules, amounts, interest terms, and default conditions. Customize it to your needs and formalize payment terms with confidence.

Somewhere between drafting, tracking, and enforcement, the payment agreement contract process breaks down. A payment date gets missed. A default clause sits buried in a folder. Collections drag on for months when they should take weeks.

Companies lose an average of 9% of their earnings due to poor contract management and value leakage—and payment agreements are ground zero for this problem. When these contracts are managed manually through spreadsheets and email chains, every single one becomes a potential revenue leak waiting to happen.

The upside? This isn’t a legal problem anymore. It’s a technology problem. And it has a solution.

Defining the payment agreement: Clarity and legal authority

Let’s start with the basics. A payment agreement contract is a legally binding document where one party (the debtor) commits to repaying a specific financial obligation to another party (the creditor) according to clearly defined terms. Think of it as the bridge between “you owe me money” and “here’s exactly how and when you’ll pay it back.”

Read also: Repayment Agreement Guide.

Is a payment agreement legally binding?

Yes, but only when it includes the essential elements. Courts recognize payment agreements as enforceable when they contain clearly identified parties, a defined debt amount, a repayment schedule, mutual agreement through signatures, and consideration (the promise to pay in exchange for debt relief or forbearance).

Without these elements, you’re holding paper, not protection.

The anatomy of a simple payment contract between two parties

At its core, a simple payment agreement contract between two parties needs four foundational components:

- The parties: Clear identification of the debtor and creditor

- The debt: The exact amount owed, including any interest or fees

- The payment plan: Specific dates, amounts, and payment methods

- Default consequences: What happens when a payment is missed

This simplicity is deceptive. The real challenge isn’t drafting these clauses; it’s ensuring they’re enforceable, tracked proactively, and activated the moment they’re needed.

Read also: 20 Essential Types of Contracts Explained

Stop leaving cash flow to chance

HyperStart CLM automates the entire contract lifecycle. Stop chasing spreadsheets and start protecting cash flow strategically.

Book a DemoThe 7 critical clauses of a secure payment agreement

A payment agreement contract lives or dies on its clauses. Here are the seven that separate a protective document from a legal liability:

1. Parties and debt identification

Name the debtor and creditor explicitly. Define the original debt amount, the source of that debt (invoice number, loan agreement, court judgment), and any accrued interest. Ambiguity here becomes your enemy in court.

2. The payment plan and repayment schedule

Specify the payment frequency (weekly, monthly, quarterly), the amount per installment, the payment method, and the total duration. If there’s flexibility built in—say, allowing prepayment without penalty—state it clearly.

3. Default and remedies clause

This is your financial insurance policy. Define what constitutes default: Is it one missed payment? Two? Does a partial payment count? Then specify your remedies: late fees, increased interest rates, or the right to pursue collections.

Key insight: The more specific your default definition, the faster you can act when it’s triggered.

4. Acceleration clause

An acceleration clause gives you the right to demand immediate full payment of the remaining balance upon default. This is your leverage. Without it, you’re stuck waiting for each installment—even after the debtor has demonstrated they won’t pay.

5. Governing law and dispute resolution

Which state’s laws apply? Will disputes go to arbitration or litigation? Who pays legal fees? These questions become expensive when answered mid-dispute instead of pre-signature.

6. Release and indemnification

Upon full payment, the creditor releases the debtor from the obligation and agrees not to pursue further claims related to this debt. This protects both parties from future disputes about whether the debt was satisfied.

7. Amendments and entire agreement

Require written consent from both parties for any changes. Include an “entire agreement” clause stating that this document supersedes all prior negotiations, preventing the debtor from claiming different terms were discussed.

Read also: General Services Agreement Essentials.

The cost of manual payment agreement management

Let’s talk about what manual management really costs.

Risk from manual tracking

Spreadsheets don’t send alerts. Calendars get ignored. Email reminders depend on someone remembering to set them. The result? Firms lose significant revenue from missed obligations and poor tracking, with some legal teams reporting that unbilled work alone can exceed $70,000 annually per attorney.

The collections drag

Here’s the math that should keep CFOs up at night: Every day a payment agreement sits in default without action is a day your collection probability drops. The average collection lockup is 45 days, meaning 1.5 months of annual revenue is tied up in accounts receivable. Top-performing firms keep this below 19 days through aggressive automation and tracking.

A study found that for one utility firm, the mean Average Collection Period (ACP) was ~309.9 days, illustrating that long collection cycles negatively impact performance.

But most organizations don’t even know they’re in default until weeks after it happens. By the time legal gets involved, you’re not collecting a debt; you’re negotiating a settlement agreement at a discount.

The comparison: Manual default tracking costs you time (legal reviews), money (collections agencies at 25-40% of recovered amounts), and opportunity (capital tied up that could be deployed elsewhere). An automated system costs a fraction of one collection case.

The template trap

Free payment agreement templates are everywhere. They’re also useless without three critical components:

- Customization for your jurisdiction: A template drafted for California law might miss key enforceability requirements in Texas

- Integration with tracking: A template sitting in Google Docs doesn’t know when a payment is due

- Default activation protocols: Who gets notified? What action triggers? When does legal escalation begin?

Without these, your template is just formatted text. It’s not a working asset.

Elevating your financial security: Automation for payment agreements

This is where the conversation shifts from “managing” payment agreements to strategically weaponizing them for cash flow protection.

From hours to minutes: AI-powered drafting

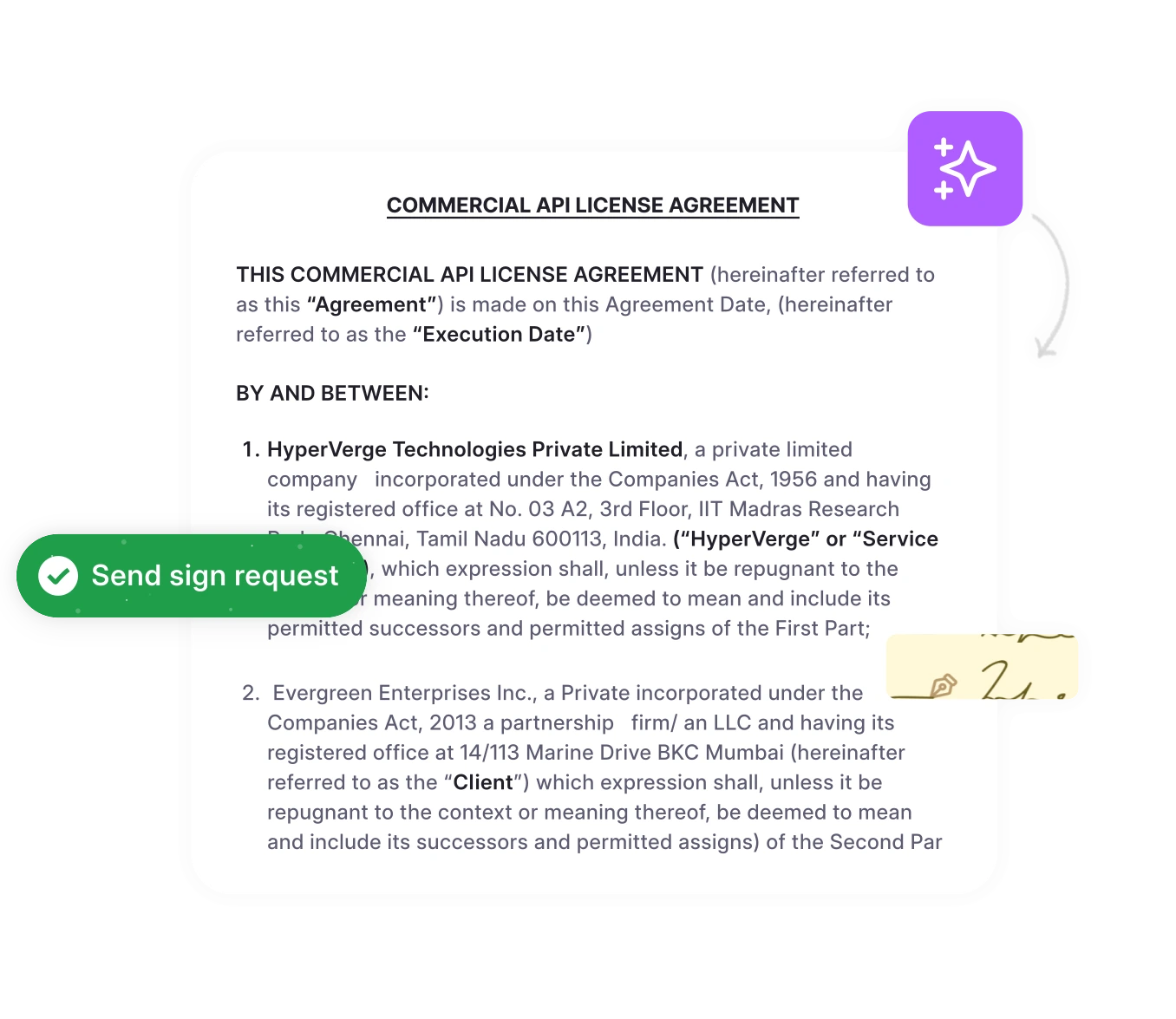

Modern contract lifecycle management (CLM) platforms use AI to generate payment agreement contracts from pre-approved templates in under 60 seconds. You input the variables—debtor name, amount, schedule—and the system outputs a compliant, jurisdiction-specific document ready for signature.

Teams using HyperStart CLM reduce contract review time by 40% and complete first-cut reviews of around 20 critical items in less than one minute.

Proactive tracking: Automating alerts for payment deadlines and defaults

Here’s how automated payment agreement management actually works:

Every stakeholder, including legal, finance, and collections, receives role-specific notifications. No one needs to “remember” anything. The system knows.

- Instant clause extraction: AI reads a counterparty’s payment proposal and flags deviations from your standard terms

- Risk scoring: The system evaluates debtor payment history, jurisdiction enforceability, and clause strength to assign a “collectability score”

- Predictive analytics: Based on past defaults, the platform predicts which agreements are high-risk and suggests proactive interventions

Streamlined enforcement: Centralized default tracking

When a default is detected, automation triggers your enforcement playbook:

- Day 1: Automated notice to debtor referencing default clause

- Day 7: Escalation to the finance team with collections recommendation

- Day 14: Legal review with litigation cost-benefit analysis

- Day 30: Pre-litigation demand letter if no response

Audit-proof repository: Secure storage and retrieval

Every version of every payment agreement, every amendment, every signature, and every payment confirmation is stored in a centralized, searchable repository. When a debtor claims “I never agreed to that,” you pull up the signed document, the email confirmation, and the payment history in 10 seconds.

Not 10 minutes digging through drives. Ten seconds.

Why this matters for payment agreements: Because when you need proof—for litigation, for audit, for internal review—you need it instantly. Manual filing systems fail this test. Automated repositories pass it.

Read also: Managing the Service Agreement: A Practical Guide

The strategic shift: Treating payment agreements as revenue protection assets

Here’s the reframe legal and finance leaders need to make: Payment agreement contracts aren’t administrative documents. They’re active financial instruments that either protect revenue or allow it to leak.

Tim Cummins, President of World Commerce & Contracting, notes that.

“Contracts are about brand image and economic performance. They are our link to the market… The solution, we believe, is the creation of an Office of Contracting… with responsibility for the quality and integrity of the contracting process”.

When you automate the payment agreement lifecycle, you’re not just saving time. You’re creating a system where every payment deadline is tracked, every default is caught immediately, and every enforcement decision is data-driven instead of reactive.

The organizations that get this right don’t just collect more money—they collect it faster, at lower cost, and with less legal risk.

The AI contract management revolution

Industry experts predict that “AI, machine learning, and automation are soon to be standard in all platforms. The tipping point is coming, and there will be few tools without AI/automation”. For payment agreements, this means:

- 90-day advance notice: “Payment #5 of 12 due in 90 days”

- 30-day reminder: “Payment #5 due April 15—confirm receipt method with debtor”

- Day-of alert: “Payment #5 due today—monitor bank account for deposit”

- Default trigger: “Payment #5 missed—activate default clause protocol”

This isn’t theoretical. It’s happening now in finance and legal teams at scale-ups and enterprises that have moved beyond manual contract management.

Key takeaways for legal and compliance teams

We live in a time when people won’t remember what a tool without AI was. The tipping point is coming, and there will be few tools without AI/automation.”

Payment agreement contracts are financial protection tools—but only when they’re tracked proactively with automations.

Here’s your action plan:

| Manual Process Risk | Automated Solution |

| Payment deadlines missed in spreadsheets | 90/60/30-day automated alerts to stakeholders |

| Default discovered weeks after occurrence | Real-time default detection and protocol activation |

| Templates lack enforceability or compliance | AI-generated contracts from pre-approved, jurisdiction-specific templates |

| Hours spent searching for contract versions | Centralized repository with 2-second retrieval |

| Collections decisions based on guesswork | Data-driven enforcement with cost-benefit analysis |

Automation doesn’t just reduce admin time. It fundamentally changes the economics of how you protect revenue.